In buying a home, people often browse through a long list of foreclosed properties trying to find the best possible deals they can get. While a lot of them might be thinking to always find cheap homes, there are those who got thought got it cheap but paid an expensive price later on. It’s not rocket science, but there are techniques and ways to find great deals. It’s difficult, but it can be done.

Elizabeth Weintraub of The Balance has posted an article on how to find foreclosures and government-seized homes. Her article is very informative and contains lots of helpful information in finding foreclosed homes.

How to Find Foreclosures and Government-Seized Homes

Image Source: The Balance

Finding foreclosures is fairly easy in depressed markets, but it’s also simple to find foreclosures in strong real estate markets. The difference between the two markets is you will find a greater number of foreclosures in falling real estate markets.

Many pre-foreclosure homes that were once offered as short sales end up as foreclosures, which are eventually deeded to the bank. The reason why purchasers may refuse to buy a short sale home could be any of the following:

Sellers stripped the foreclosure home’s assets and/or vandalized the property.

The bank refused to accept less than its present mortgage balance.

Buyers passed by the short sale in favor of a hassle-free purchase.

The location of the home and/or neighborhood was undesirable.

The listing was overpriced at its mortgaged amount.

The seller did not qualify for a short sale.

Finding and Buying Foreclosures

Not every foreclosure is a great bargain, and some can morph into unexpected nightmares. There are drawbacks to buying foreclosures. Some foreclosed homes are diamonds waiting to be polished. Inexperienced foreclosure buyers might want to hire a real estate agent for guidance and assistance. There are several ways to find foreclosures, described below, whether you work with a real estate agent or not.

Real Estate Agents

The top-producing agent in Sacramento specializes in listing foreclosures. We know who he is because we know how to enter the search values in the Multiple Listing Service (MLS) to bring up all the foreclosures. Consumers do not get direct access to the MLS like agents do.

You can ask your buyer’s agent to search for REOs (real estate owned by lenders), and when you see a listing agent’s name over and over, pull up that agent’s profile and look at his or her listings. You will probably find a ton of foreclosures at your fingertips.

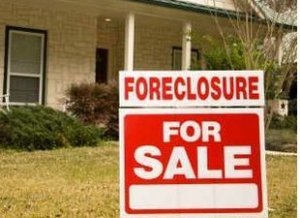

Real Estate Signs

Driving through distressed neighborhoods where you want to buy is another great way to find foreclosures. The signs might read:

Foreclosure

Bank-Owned

Bank Repo

Call the agent whose name is on the sign and inquire about other foreclosure listings that may be coming on the market. Agents who specialize in foreclosures sometimes wait weeks while bank management approves the list price, so you can get a jump on other buyers by asking about new foreclosures not yet listed. If you are working with a buyer’s agent, you can ask your agent to obtain this information for you.

Major Bank Websites

Many banks maintain online lists of foreclosed properties. Not every bank will sell to individual buyers. A more common practice among the large lenders to dispose of REOs is to bundle them into a package and sell that package at a discount to investors. Read the rest of the article here…

As a very good reminder from the experts, foreclosed properties does not all the time means a good bargain, some can even expert the worst. There are basically lots of risks to be minimized. However, there are also those properties that are like great deals. If you aren’t confident with your knowledge and skills in scanning through the foreclosed list, you can always seek the help of an expert real estate agent for some guidance.

However, if you’re eager to do things on your own, you need to have at least the basic knowledge on how to become successful in finding good deals at foreclosed properties in Baltimore. You need an expert tip, and Maryland Properties posted very helpful tips in buying foreclosed properties that you might want to consider. Refer to the awesome tips below:

5 Tips for Buying a Foreclosed Home

Image Source: Flickr

Home buyers who are looking for discounted properties this summer may consider a foreclosed property. The conventional wisdom being that banks and lenders will offer steep discounts to unload their property and great deals are to be had. However, foreclosures offer their own challenges and in their online article 5 Tips for Buying a Foreclosed Home, Fox News explains some of the differences you may need to consider if you are considering buying a foreclosure.

The “As-Is” Sale

Disgruntled homeowners in foreclosure can feel like they have nothing left to lose. Faced with the prospect of losing their house, homeowners sometimes leave the place stripped of anything valuable or useful, including door knobs, fixtures and wiring. In cases like this, the lender is unlikely to make repairs and will sell the home as-is. While you can get the place at a steep discount, it might only be a bargain if you’ve got some DIY skills. This shouldn’t necessarily discourage you from buying, but you’ll need to figure out if the cost of repairs will offset the discounted offer price. Also consider a mortgage that will allow you to borrow the cost of the repairs such as an FHA 203k loan.

Not Knowing What You’re Getting Into

With most homes, you’ll likely get some disclosure from the current owners. A helpful homeowner might give you a little advice, like the best place to start a garden, or offer you a heads up on minor repairs, like a bathroom door that sticks. And when it comes to big repairs, such as a shoddy foundation or termite damage, the owners might be legally required to let you know before you buy the place. But a lender has no history with the home, so don’t expect to get a run-down of problems before you move in. A foreclosure might be a good deal, but it can also turn into an unexpected adventure.

Don’t Assume They’ll Take Any Offer

While a foreclosed home can often be a bargain, you shouldn’t expect the lender to accept a lowball offer. Even in a market flooded with foreclosures, a bank might balk at a low offer, preferring to wait until housing prices bounce back rather than take a huge hit on the investment. However, you can use local foreclosures to your advantage. Take a look at recent sale prices for homes sold by lenders — which are often called real-estate owned, or REO sales — to help you price the place.

It Takes More Time

Most mortgages are backed by big banks and financial institutions, which means you will likely run smack into a large, slow-moving bureaucracy when trying to buy a home in foreclosure. With a traditional home sale, you can expect to find out if your offer has been accepted within a day or two. But when buying from a financial institution this process can take weeks. So have patience and don’t freak out if you don’t immediately hear back from the seller.

Those tips will absolutely help you fully understand and have a grasp on how finding and buying good deals in foreclosed properties. Don’t be shy to ask important questions before signing and completing the purchase. Expect these foreclosed properties to require minor (even major) repairs, might as well bring a home repair expert to know the repair cost.

When you’re confident enough in your skills and judgment and does not need the help of an expert real estate agent, then these guides written by Cynthia McIntyre at Baltimore Fishbowl will definitely help you in landing a new home in Baltimore. Check out the guides below:

Sold! A Step by Step Guide to Buying a House at Auction

Image Source: Baltimore Fishbowl

If you’re serious about this, you may already be checking out auction properties — on the A.J. Billig website for local real estate, or Auctionzip.com and RealtyTrac.com for real estate nationwide. Public foreclosure auctions of bank-held real estate, sometimes called Trustee’s Sales, are the most transparent, least complicated type of real estate auction, and that’s what this article is about. Tax auctions or short sales are better left to buyers with real expertise or professional advice. That said, getting a realtor who’s knowledgeable about foreclosures can be a plus in any situation.

If you’re only half serious, and you’ve simply just spotted an interesting property, what’s the first step? “Call the auctioneer,” says Billig. The name will be on the sign or in the ad. He points out that Billig now offers QRC or “quick response code” — basically a bar code on the sign itself that you can scan with your cell phone and get right to the web page to get information on the property.

OK, Step 1, call the auction house to get the date and location of the auction, terms of sale, and a time to view the property. AUCTION SALES ARE “AS IS.” You need to get in there with a contractor to look around and see where the problems are. Almost always, it’s roof, plumbing, heat and AC. This part needs to happen fast, three weeks is probably the maximum, a few days is common. It would be great to have a contractor on-call, and a lot of them are not too busy these days. Now, get online and start researching the neighborhood — the average house price, the quality of the local schools, the rental market and the property taxes. Be sure to drive by the property again, to get a further idea of the neighborhood. There’s always the chance of a casual meeting with the owner (and possible last-minute deal before auction) or neighbor (with some insider information to help your bidding decisions). Take pictures and notes, but be discreet, as the owner may still be living in the home!

Once you’ve lined up a viewing and done your research, know that if you place a bid and win, you will be required to put down roughly 10% in cash or cashier’s check immediately — like as soon as the gavel goes down. The rest needs to be paid by a specified date, usually in about 30 days. If it’s not paid, you lose the deposit.

So Step 2, organize the financing. Unless you can pay the full amount in cash, in which case all you need to do is get a cashier’s check for roughly 10% of what you plan to bid, you’ll need financing. This needs to be worked out ahead of time with your bank, because especially now, you can’t assume the credit will be there, and unless you are deemed totally credit-worthy, banks are more reluctant to lend money to buy a house in foreclosure. One reason for this is that auction deposits are not refundable, should something go wrong.

Step 3, — and everyone agrees on this — get a title search. While Billig guarantees that there are no hidden liens on their houses — in other words, no money owed by the owners that the new buyer will be obligated to pay — you still need the advantage of a title search. Betsy Jiranek, a Baltimore title agent whose company, American Land Title Corporation specializes in title searches, explains it this way, “we make sure you are getting the title ‘free and clear of all liens and encumbrances.’ We search land records, tax records and house history, looking for bankruptcies, wills, anything that could endanger the free passing of the deed.” This is public information, she reminds me, but most people are not comfortable researching and interpreting all the documentation that’s out there. Normally, a title search takes a week, she says, “but in a pinch we can turn it around in a day.”

Step 4, get title insurance. “Ninety-nine times out of a hundred, everything is fine,” says Jiranek, “but title insurance is for that last one percent.” In the words of Dan Billig, “ I would absolutely get it (title insurance). It’s so cheap, you’d be foolish not to.”

Step 5, determine your bid amount. Unless there is a minimum bid requirement, a safe bet is at least 20% below market value, and as far below that as you think you can go, considering local real estate conditions and the properties potential for increasing in value with repairs and improvements. You’ll want to gather the following information:

Outstanding balance on the mortgage

Estimated market value

Other liens and loans the owner may have taken out

History of ownership (if it was owned by a contractor or corporation, it maybe less of a bargain than a distressed homeowner)

Your monthly expenses as the owner of the house – mortgage payment, taxes, insurance, repairs, etc

Following these guide could allow you to at least find good deals on the list of foreclosed properties in Baltimore. While doing it on your own bring more risks than with an expert broker, it’s more rewarding since you don’t have to pay extra. Keep in mind these guidelines you’re in good hands.

As mentioned a couple of times in this post, buying foreclosed properties in a risky, but rewarding thing to do, especially if you hit the jackpot and find the best deal. While you can do it on your own, it is always recommended to seek the help of an expert broker to avoid any hidden costs such as additional repairs. If you want to move into Baltimore and is looking to buy foreclosed properties in the city, Dependable Homebuyers are here to help you. Visit https://www.dependablehomebuyers.com for more information and start your home buying journey.